")

Subdued holiday season offers opportunity for service improvements

On-time delivery inching back toward pre-pandemic levels

(Photo: Jim Allen/FreightWaves)

The winter holidays have long been harbingers of chaos for the logistics industry. Typically, volume spikes and tender rejection rates soar ahead of the festivities, leaving shippers scrambling for capacity as shoppers scavenge store shelves for the latest and greatest gifts.

Last years peak retail season stands apart from previous years in that there wasnt much of a peak at all.

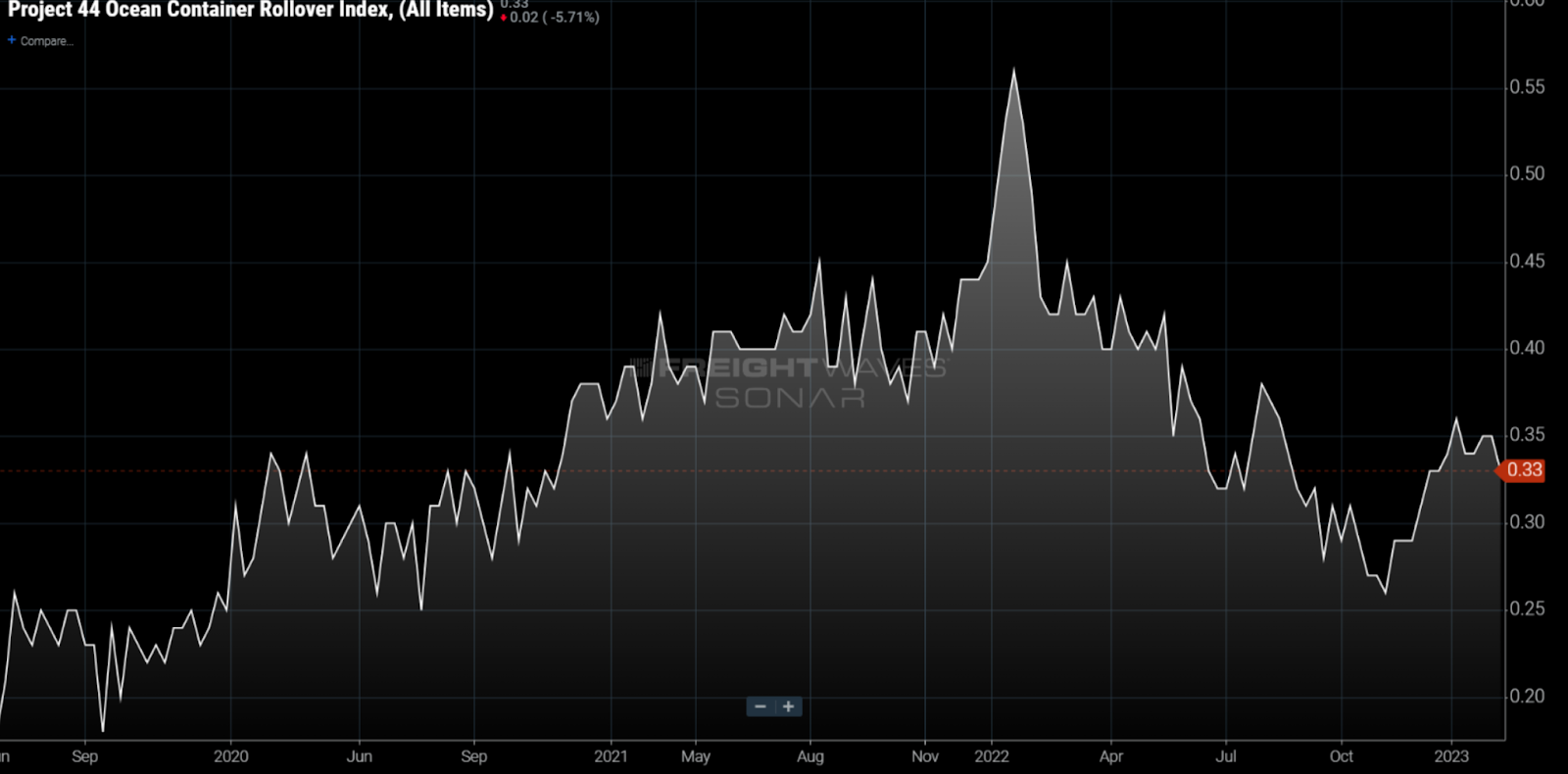

The project44 Ocean Container Rollover Index (P44ORI) which measures the weekly proportion of cargo departing a port on a different vessel than originally scheduled shows that rollovers have been suppressed on a year-over-year basis for quite some time.

Lower rollovers mean fewer shipments are being pushed to later sailings due to packed ships. Generally, this indicates fewer delays, loosening capacity and falling rates. While rollovers did jump slightly around Christmas, they are quickly returning to pre-holiday levels.

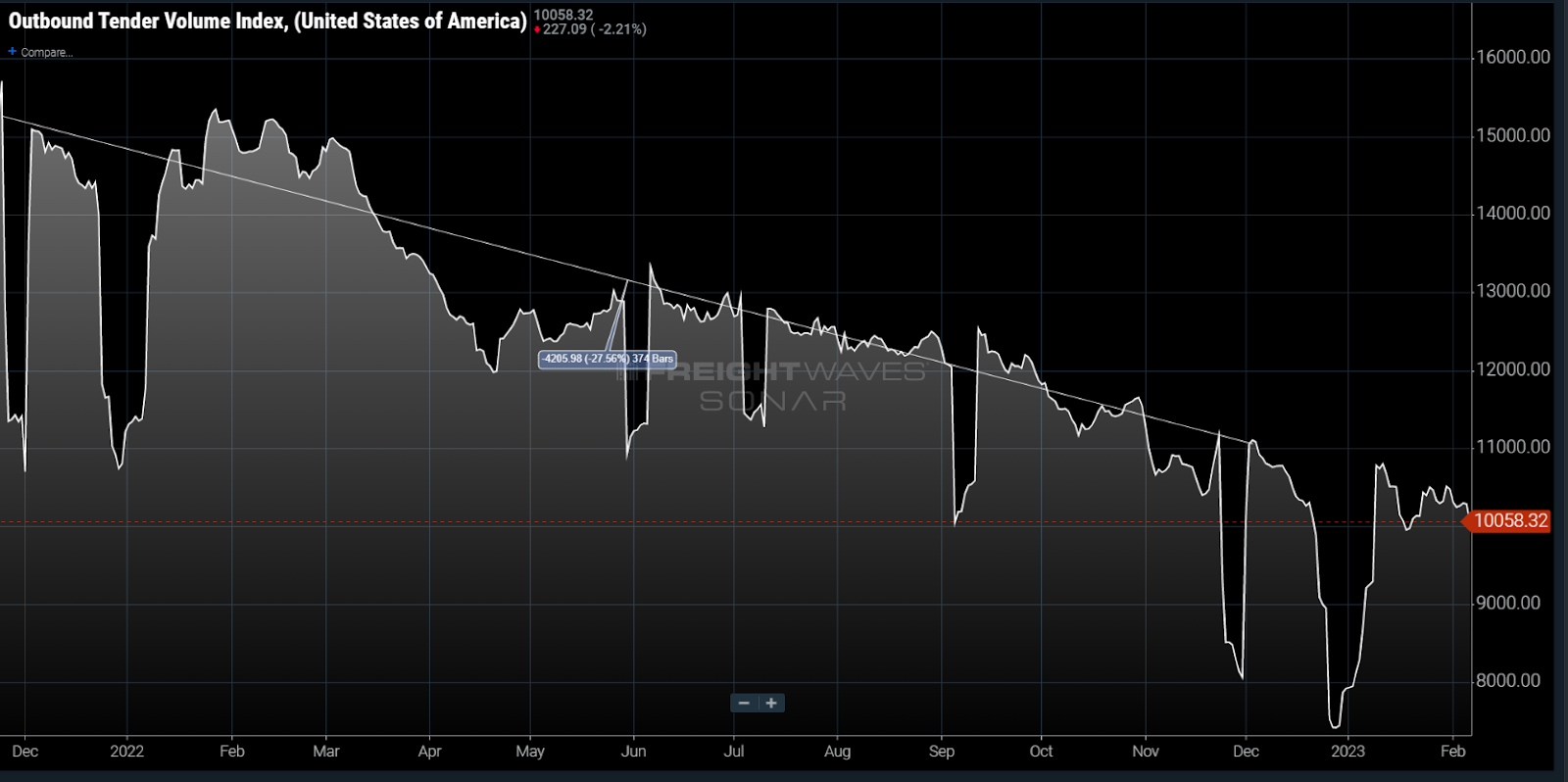

SONARs Outbound Tender Volume Index (OTVI) paints a similar picture in the trucking space. The index measures electronic offers from shippers to truckload carriers on a real-time basis. An increase in OTVI indicates higher volumes and tighter capacity, while a decrease in OTVI points to lower volumes and looser capacity.

Outbound volumes fell nearly 30% between December 2021 and December 2022, indicating a less intense peak season than those seen in previous years. This weakening was especially stark compared to the 2020 and 2021 peak seasons, which were characterized by coronavirus-fueled volatility.

Tender rejections which have been trending downward for several months also remained depressed throughout the festive season. In fact, SONARs Outbound Tender Rejection Index (OTRI) stayed below 6% during the week of Christmas for the first time in the indexs history.

Every holiday season over the past five years, rejection rates have risen above 14%, FreightWaves Market Analyst Zach Strickland reported in January. The softest year before this one was 2019, when the OTRI topped 14.3% on Christmas Eve.

At the same time, FreightWaves National Truckload Index shows that rates were down over 20% year over year during the holiday season.

The National Truckload Index and the project44 Ocean Container Rollover Index closely mirror each other, further underlining the fact that lower demand, loosening capacity and falling rates are affecting various segments of the transportation industry.

All of these factors add up to create a peak season that never really hit its stride, thanks, in large part, to the easing of pandemic-era demand hikes and other shifting macroeconomic factors.

Rapid demand erosion resulting from overstuffed inventories and eroding consumption coming out of an overstimulated goods economy are the main factors driving the weakening transportation markets, according to Strickland. Those conditions are forecast to persist through the first half of 2023 at a minimum.

Plenty of financial concerns come along with a weakening market, but there is also room for opportunity with this downward pressure. Those working in the parcel space, in particular, were hit hard by pandemic-fueled online shopping trends. As demand tapers off, companies are able to spend more time and energy improving service factors like on-time performance and click-to-delivery times.

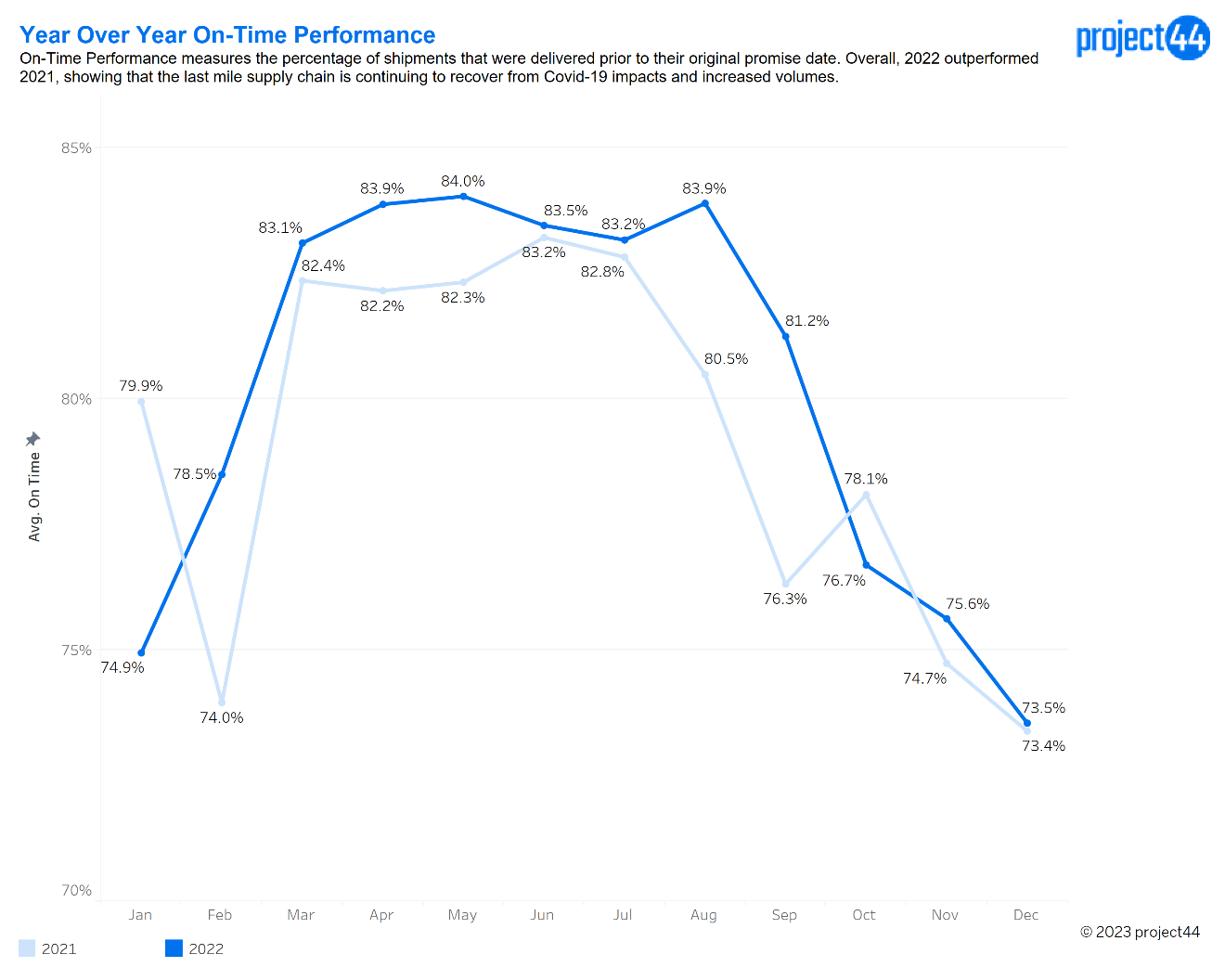

Data collected by project44 shows a steady improvement in year-over-year on-time delivery performance throughout the majority of 2022.

COVID-19-related factors caused on-time performance to suffer beginning in 2020. Pre-COVID, levels were consistently 85% to 90% outside of peak season, which runs from November through January. Since COVID-19, numbers have ranged from 70% to 84%, project44 Data Analyst Jenna Slagle said. In 2022, OTP continued to inch back up towards pre-COVID levels, but there is still a 6% difference between the pre-COVID max of 91% and the 2022 max of 84%.

This cannot be entirely attributed to a weakening market. Retailers made operational shifts in response to pandemic-fueled headwinds that are continuing to pay off, even as the market cools.

By tracking carrier diversification over time, project44 discovered that retailers increased the average number of carriers they depend on for their last-mile business by over 40% climbing to about six carriers per account.

While the market is still dominated by a few major shippers, this has allowed some smaller companies to gain traction and growth in this leg of the supply chain, Slagle said. The shift towards more carriers is one of the reasons for the steady increases in on-time performance.

A combination of factors including diversification, operational improvements and market changes is creating a more efficient, streamlined parcel space. This shows continued steady on-time performance improvement as the logistics industry inches toward a post-pandemic normal.

While a peak season mitigated by lower volumes and looser capacity creates financial stress for carriers and raises concerns about widespread economic health, this slower-than-expected time period has offered several companies particularly those in the parcel space the reprieve needed to drive service improvements after a couple of whirlwind years.